The rise of remote working in recent years, particularly in 2021-22, has affected sectors across the board. However, the pandemic has had a significant impact on the BFSI sector. Furthermore, consumer expectations continue to rise, and new technology and stringent laws are just the tip of the iceberg for banks and insurance businesses to contend with, which is why the no-code for the BFSI industry is preparing the way for a big transition.

Let’s see how it goes!

The banking, financial, and insurance services industry is one that will never end! Major macroeconomic elements are dependent on it, as are many other industries that function as a result of the BFSI sector. It is critical for banks and insurance businesses to reimagine, rethink, and adapt their business models.

Banks must digitally change and integrate their whole systems, from simple activities like e-banking, transactions, and bank statements to cybersecurity, online payment solutions, and identification.

Customer experience is a significant priority in the BFSI industry. To become an agile, efficient, and collaborative organisation, you must provide excellent experiences to your clients and customers across your business network and secure both a functional and competitive edge.

The BFSI Digital Challenge

Every minute presents a challenge for the BFSI industry, from security to customer service. The top 5 issues that hinder banks and insurance businesses’ digital transformation have been identified. We think that in order to successfully implement change, it is important to start with an organization’s deeply ingrained systems, which are typically its most fundamental, straightforward operations.

Form-filling, keeping track of transactions, and accounting procedures are huge difficulties to carry out perfectly with traditional methods and systems. In addition, managing the constant influx and outflow of data makes it nearly hard to keep track of things, and security concerns also arise.

To begin with, the BFSI sector’s obstacles and key points are

1. Manual Methods

In the BFSI sector, distrust results in manual operations, although the danger of errors does not decrease. The continued use of manual documentation by banks and insurance companies has a significant negative influence on corporate operations. Especially how long it took, how big it was, how accurate the data was, and how much it cost!

2. Paper-based Documents and Forms

Simply said, it goes beyond manual tasks! The industry uses a tonne of paper—registration papers, claims, bank forms, and checks are just a few examples. Due to the degradation in processes caused by paper forms, we do refer to this as a gigantic pest fest. Finding them in the wrong location, filing them, and, well, the coffee stains won’t disappear on their own!

3. Safety

Although it can seem obvious sense, securing networks and software within an organisation presents significant difficulties for many businesses. Cybersecurity also becomes antiquated like traditional systems do. Any flaws in the team or the system might easily lead to security holes in the banking and insurance systems.

4. Requirements

The BFSI industry must stay up to date on regulatory compliance practises and adhere to the rules. Different departments and executives must supervise, monitor, and approve tasks and procedures.

With paper forms or antiquated technologies, obtaining a really end-to-end insurance quote, binding a policy, and managing policy administration may become incredibly onerous for insurers.

Regulations for banks that rely on spreadsheets and administrative procedures are begging for chaos. Resource-intensive compliance and regulatory organisations frequently rely on their capacity to correlate and assemble data from many sources.

5. Customer Experience

Delivering a truly customer-centric, comprehensive consumer experience is a significant and critically important challenge that the BFSI Sector faces. The modern consumer is more knowledgeable, conscious, and tech-savvy than ever before. They want personalisation and ease from their banking and insurance experiences, demand constant contact, and are actively involved in every stage of the process.

Due to the internal difficulties the BFSI sector encounters, it is frequently quite haphazard for businesses to provide an omnichannel experience that is also tech-savvy. The main reason why customers are not satisfied and remain loyal is outdated technology.

It can be quite difficult to chart a clear and truly experiential course forward with so many BFSI industry difficulties to deal with and understand. However, we have a solution that will ‘insure’ your path to digital transformation. In 2023, no-code for BFSI can succeed and completely change the sector.

Take notepads, because we’re about to share some strategies for empowering your company and “banking on” brilliance.

Using No-code for BFSI to invest in and for the future.

We cannot overstate how crucial it is for BFSI organisations to be more adaptable, deliver services faster and under better control, and foster a seamless client experience. The first stage in undergoing a digital transformation is to digitise business processes, which every bank, insurance company, and provider of financial services must accomplish.

True end-to-end digitalization will promote frictionless growth in addition to enabling and removing operational and IT problems. from cross-selling to payments, from onboarding to loan origination that spurs growth. And with just three words and countless possibilities—No-code Applications—all of this is doable.

What is No-Code?

Simply put, no-code process automation automates operations without the need for prior understanding of programming. It is essentially the use of no-code apps to automate operations. It simplifies process automation and workflow automation.

The initial foundational steps toward offering a seamless workplace operation and digital experience are no-code applications.

The term “no-code” refers to application development platforms that automate procedures that require no coding! This means that apps can be constructed entirely through visual, intuitive interfaces, without the requirement for programming knowledge. These platforms frequently provide simple features, such as drag-and-drop form builders.

They function in the same way that you may make a collage with stickers; simply take what you need and place it where you need it the most. It does not require any coding. These apps aid in the rethinking, repurposing, and innovation of everyday operations and manual processes.

It also allows for simple and smooth integration with numerous tools. We won’t lie no-code apps unleash the power of what your managers and executives do in the form of citizen development, or anyone who produces an app without any technical experience.

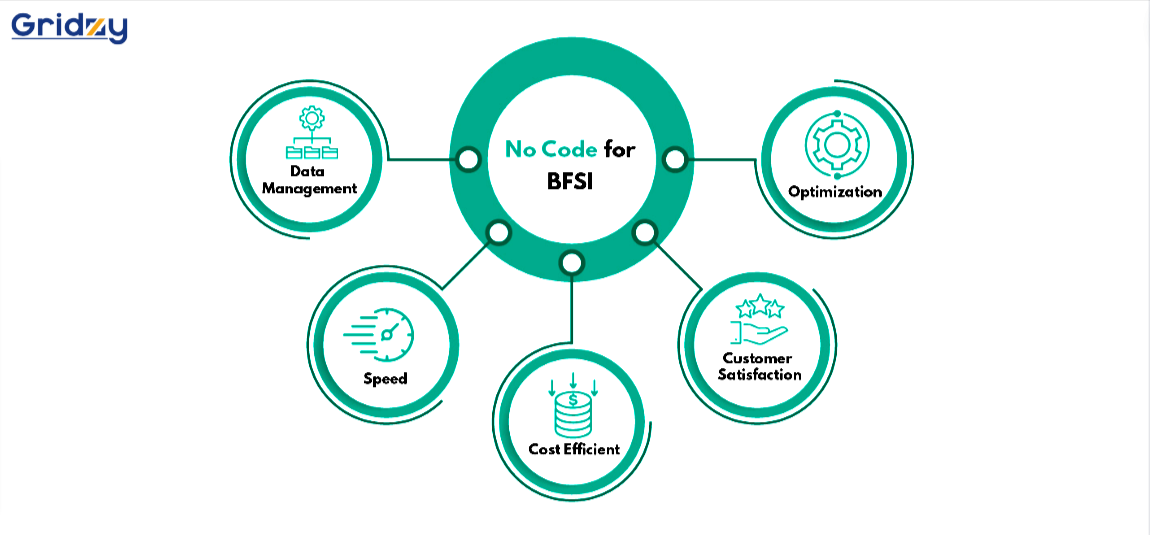

But why precisely No-Code for BFSI?

Today, however, with digital transformation transforming every industry, there is a greater need than ever for a digitally connected BFSI sector. Even while businesses would like to turn into digital businesses, they are unable to find or afford top-notch tech employees who can handle all of the necessary IT tasks. This demand is taking advantage of these organisational pain points.

However, no-code application creation claims you don’t require coding experience or a background in IT.

Allowing your workers to create apps and modify them as needed (citizen developers) without prior technical knowledge or the need for training is all that is required to tackle the digital challenge.

Banks and insurance businesses can now adapt no-code for BFSI to meet their specific requirements while still having the ability to develop quickly. The development and delivery of ground-breaking solutions using no-code apps is up to 10X faster since they handle all the underlying complexities, including database, UX, security, and integration.

No-code for BFSI industry makes sure they can react quickly to requests from the company and customers. Because they provide all the necessary technical infrastructure and skills to construct a variety of apps, from onboarding to tracking transactions and security, no code for BFSI organisations is ideal.

To begin, a few No-Code for BFSI Sector: –

1.Finance Administration

Budget spreadsheets based on Excel can be readily eliminated, and transactions and approvals can be automated and optimized. Useful apps can automate the deposit and withdrawal processes.

2.Loan and Investment Management

You’ll save a tone of time by automating and simplifying loan requests and investing accounts! Through automated workflows that follow company procedures and policies, quick approvals can be ensured. And what’s this? Utilize sophisticated reports and dashboards to analyze investment strategies and monitor cash flows over any time period.

By automating data processing, your bank may literally avoid performing manual calculations and number crunching before making a loan decision.

3. Portals and Services for Banking

Everybody is familiar with how banking portals appear. You may actually create and provide your customers with an end-to-end banking portal with no-code for BFSI. By establishing a core banking system, customers may manage their transactions and funds with ease. Since no-code apps prioritise the user experience, you’ll notice quicker processing and updated data on the portal right away. Using online forms and approvals, you may do away with manual processing and pointless bank trips.

4. Claims Administration

Create robust databases using apps that are driven by no-code. Create apps that can be customised to follow company guidelines for managing finances and budgets. Keep client information and contract archives that enable managing claims and establishing recurring renewal reminders.

5. Onboarding of Customers

Financial lenders can benefit from no-code solutions by speeding up the onboarding and offboarding of customers. The time spent on laborious KYC procedures can be drastically decreased with the automation of these processes and custom applications; this is in addition to allowing for simple data updates and the removal of errors.

6. Meeting Regulatory Requirements that are Changing

No-code the quick-change management of regulatory requirements can be assisted by citizen development. Simple upgrades and quick application development allow for each new modification in the process and avoid any potential obstacles.

Empowering No-code for BFSI with Gridzy

A cutting-edge no-code platform called Gridzy empowers the BFSI industry and makes automation possible. We collaborate with clients to create automated systems that are quick, effective, and code-free. Through the coordination of human and machine talent, as well as the injection of insights and efficiency from data, clients accomplish results.

As a platform, Gridzy firmly believes in and pledges to transform every process for BFSI, increasing productivity and efficiency.

With an emphasis on creating streamlined collaborative banking and financial services, we have created and deployed solutions for leading financial services firms.

Conclusion:

Gridzy is a top no-code application development platform and gives BFSI clients end-to-end digital solutions. No-code application testing with Gridzy is a reliable, high-impact solution that makes use of in-built technological experience and skills as well as a thorough understanding of customer requirements. It resonates with the requirements of the moment and is both efficient and practical. Deployment, management, and rollout are also quicker and simpler than you might anticipate.

FAQ

Q1. Which 7 BFSI trends are there?

Consumers Will More Frequently Prefer Digital Channels Over Contact Methods

Banking is becoming into a customer-focused industry.

Open Banking Puts More Pressure on the Market

AI Will Improve Banking Through Chatbots and Virtual Assistants

Greater emphasis on big data and analytics

The Evolution of Banking Apps as Digital Assistants for Users

More people will feel comfortable doing their own banking.

Q2. Why are BFSI Industries moving forward with integrating chatbots into their internal processes?

For the interest of the company, chatbots and PC programmes use the content-based live visit as an interface to do errands for customers. They are working on a low-cost way to present AI while yet keeping the money.

New, digitally savvy businesses have found success in luring customers with donations that are simple to comprehend. Heritage banks believe that investing in and receiving authentic items is difficult.

These huge banks need to modify their standard operating procedures in order to stay focused. They achieve this by integrating more mechanical autonomy in account management, which will appeal to clients with greater education.

Q3. What Is a Chatbot?

A chatbot is a computer-based program intended to emulate discussions with human clients on the web. Utilizing AI & robotics, a chatbot can help clients without the need for a client administration specialist on the opposite end.

Learn More: – Is No-Code technology the blockchain of the future?